We buy houses for cash in Orange County the easy way.

Sell your home 'as is.' We renovate and resell it, sharing the excess profits with you.

Hear what our customers have to say about us.

Why Orange County homeowners trust FlipSplit home buying process.

Ready to sell fast?

Sell as-is and get the best price. No repairs, no showings.

What people are saying...

Learn why thousands of people have requested offers from FlipSplit to sell their home.

“Almost everything about this process was quick and painless. Relocating halfway across the country and being on a strict timeline made this... Read More

Anaheim, CA

“Easy, quick, transparent transaction. Did everything they said they would do. Excellent communication start to finish. Oh wait, we may not ... Read More

Anaheim, CA

“Overall very easy and stress free process. They took the work out in trying to prepare the house for resale and they offered me a very fair... Read More

Anaheim, CA

“The FlipSplit team handled everything with professionalism and care. They took the stress out of selling my home, and I couldn’t ... Read More

Anaheim, CA

“Almost everything about this process was quick and painless. Relocating halfway across the country and being on a strict timeline... Read More

Anaheim, CA

“Easy, quick, transparent transaction. Did everything they said they would do. Excellent communication start to finish. Oh wait, w... Read More

Anaheim, CA

We Help Homeowners sell quickly in Orange County

We help homeowners sell their house fast in Orange County sell as-is in these cities:

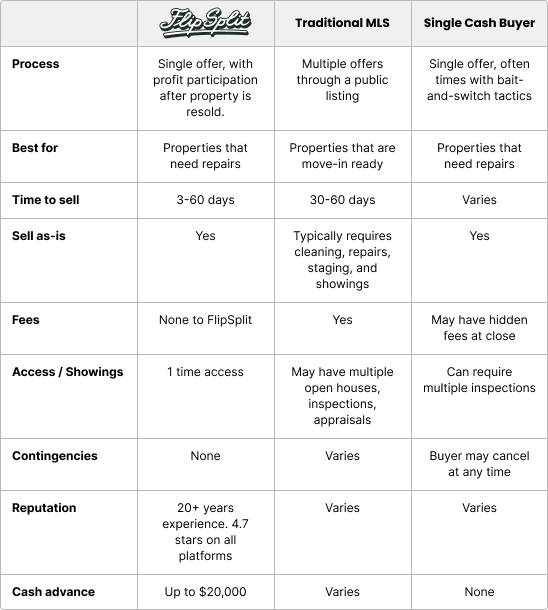

When to use FlipSplit

We're Here to Help Sell Your Southern California Home

Any property in 'as is' condition.

Inherited property

Relocating out of state - need to move quickly

Financial distress - Avoiding foreclosure

Property in good condition but want a quick sale

Downsizing into a smaller home

Deferred rental property you want to get rid of.

Code Enforcement Violations

1031 Exchange

Bank owned REO liquidation

Deferred rental property you want to get rid of.

Need to sell existing house to buy your new house

FlipSplit Benefits: sell your house fast

No Realtor Fees & No Closing Costs

When you sell your Los Angeles house to us, you don’t have to worry about paying realtor fees or closing costs. We take care of all the paperwork and logistics, covering all the costs associated with the sale. This means you can keep more of your hard-earned money and avoid the hassle of dealing with real estate agents. Selling your house has never been easier or more cost-effective.

Sell Your House As-Is, No Repairs Needed

We buy houses in any condition, which means you don’t have to worry about making repairs or renovations to sell your property. We take care of all the repairs and renovations, so you can sell your house as-is and avoid the hassle and expense of fixing it up. Whether your house is dated, distressed, or in need of major repairs, we are ready to make you a fair cash offer and handle the rest. Selling your house as-is allows you to move forward without the stress and financial burden of home improvements.

After record-high demand throughout the COVID-19 pandemic, recent reports indicate the Orange County housing market is experiencing declines due to increasing mortgage rates. As everyday costs continue to rise, prospective buyers have become more hesitant to take action. Despite higher interest rates, however, overall demand remains strong, coupled with a low inventory of available homes making for a lucrative seller’s market.

The median home price in Orange County recently exceeded the $1 million threshold, making it the most expensive county within Southern California. Fewer and fewer homes are going on the market, leading to fierce competition amongst buyers, only driving up home prices even further. Additionally, a higher-than-average household income across many Orange County residents allows for even greater purchasing power.

Despite racking up well above-average median home prices, Southern California boasts some of the lowest property tax rates in the U.S. According to SmartAsset, the average property tax rate in Orange County hovers around 0.69%, though this number can vary by neighborhood. Learn more about navigating OC property taxes in our guide to Orange County real estate taxes.

Several economic indicators are showing signs of a housing bubble in the Orange County real estate market, with housing prices skyrocketing at a pace far greater than people’s income. Several first-time home buyers are getting beat out by multiple offers above asking price, making an already expensive market even more unattainable for most buyers. Though mortgage rates aren’t expected to swell as they did during the last housing crisis, it’s clear that the housing boom of the last few years isn’t sustainable, and experts expect the Orange County real estate market to correct itself in the coming months or years.

Cash home buyers in Orange County offer one of the fastest ways to sell a house. A local cash home buying company can make a cash offer for your home within 24 hours, buy houses as-is, and close quickly, often in days instead of months. This is ideal if your house needs repairs, you need to sell quickly, or you want to avoid the hassle of owning that house any longer. Selling directly to a cash buyer eliminates agent commissions, showings, and financing delays, helping you sell your Orange County home fast for cash with certainty.

For many homeowners, selling a house for cash is the easiest way to sell. Traditional listings require preparing a house to sell, fixing up your house, hosting open houses, and having people walk through your house. With local cash buyers, you can sell your home as-is, avoid the hassles of open houses, and skip months of uncertainty. If you want to sell your Orange County house quickly and without stress, a cash sale offers a simpler, faster alternative.

The best companies that buy houses in Orange County are local cash buyers with a proven track record, transparent pricing, and the ability to buy houses directly. A reliable Orange County cash home buyer will help you sell your home quickly, provide fast cash offers, and explain the house buying process clearly. Look for a company in Orange County that is serious about buying houses anywhere in Orange County, offers fair valuations, and is ready to buy right without hidden fees.

Yes. Cash home buyers in Orange County specialize in buying houses as-is, even if the house needs repairs or major updates. If you need to sell fast and don’t want to spend money fixing up your house, a local cash buyer can buy your house in its current condition. This is a practical option for homeowners who want to sell directly, avoid renovation costs, and get a fair cash offer without delays.

The fastest way to sell your home in Orange County is to work with a local cash home buying company. These buyers can make an offer on your house within 24 hours and close on your timeline. If you’re looking to sell your house for cash, need to sell quickly, or want a fast cash offer without the traditional selling process, this approach helps homeowners across Orange County move forward with confidence.

How FlipSplit works

Sell Your Southern California Home in 4 Easy Steps

Provide Property Details

Southern California homeowners can conveniently submit their property information online, including the property address, to FlipSplit.

Property Inspection

FlipSplit will conduct a 15-minute virtual or live inspection of your home. This will help us to determine an exact price we are willing to pay for your home.

Close On Your Timeline

You can choose a closing date that suits your needs, ensuring a smooth transition. Leave behind any unwanted belongings or junk, while making no repairs. We take care of ALL of that.

Participation Results

We’ll work on renovating and reselling your house fast for the highest possible value. If our resale price exceeds the initial projections we provide you, we’ll send you 50% of the additional proceeds!

Ready to FlipSplit your home?

A Trusted Solution for Southern California Homeowners